Credit Risk Analysis: Predict If A Credit Card Holder Will Pay Dues On Time Using Terno AI

Overview

Credit card companies need to decide whether to approve credit card requests from a new customer. But since doing a hard check affects the credit score of the customer, they are not willing to do that. We aim to build a predictive model using Terno AI that determines whether the customer will pay dues on time. Using this model, the organization can decide whether to approve a credit card request **without **affecting the customer’s credit score. Check out the prompts used for this study here.

Table of Contents

Overview

Dataset

Objective

Terno AI

Our Approach: From Data to Decisions

Insights & Findings by Terno AI

Key Predictive Factors

Recommendations by Terno AI

Conclusion

Dataset

We chose the dataset below that fits our criteria from Kaggle.

Objective

To identify **risk customer** profilesTo predict if a credit card holder will default on their credit

Terno AI

Terno AI is a secure, conversational AI-powered data scientist that enables quick and precise insights through natural language, customized to your data. It’s an effective solution for saving our time and valuable resources. Terno AI builds an end-to-end pipeline from data cleaning to model generation just by taking simple prompts as input. It’s a **game-changer **in the field of data science.

Our Approach: From Data to Decisions

Finding Dataset

Data Cleaning & Pre-processing

Exploratory Data Analysis

Prediction Model

Evaluation

We asked Terno AI to generate insights and build a pipeline for our use case by using the following prompt:

Prompt: Use this dataset to understand the factors contributing to credit card approval, and build a prediction model to predict if we will be approved for credit card, evaluate the model, give all the key findings as detailed notes with numbers. If the data set is imbalanced, then make it balanced and then train the model so that we get good results on evaluation. All the findings and charts, visualizations, graphs should be neatly formatted with no cut over edges and overlapping texts.

Terno Response:

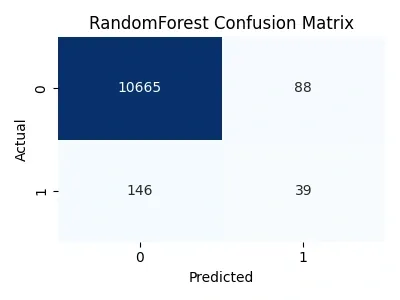

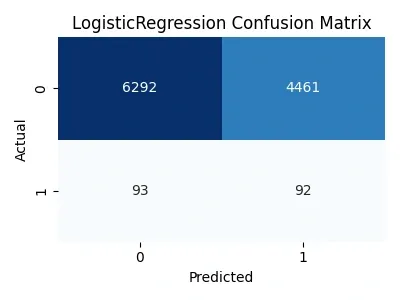

Next, we evaluate the models and compare the efficiency of the two models.

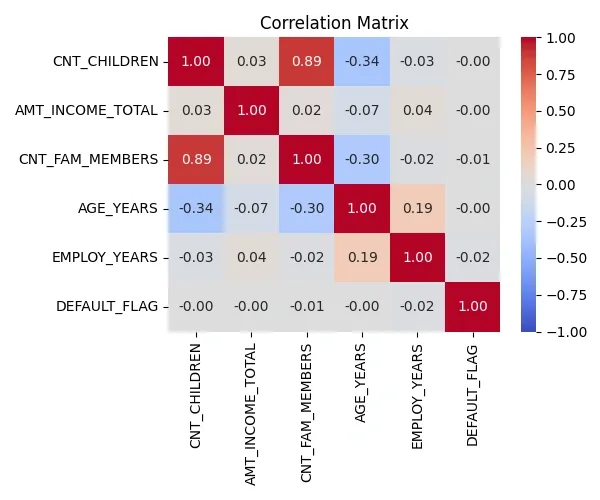

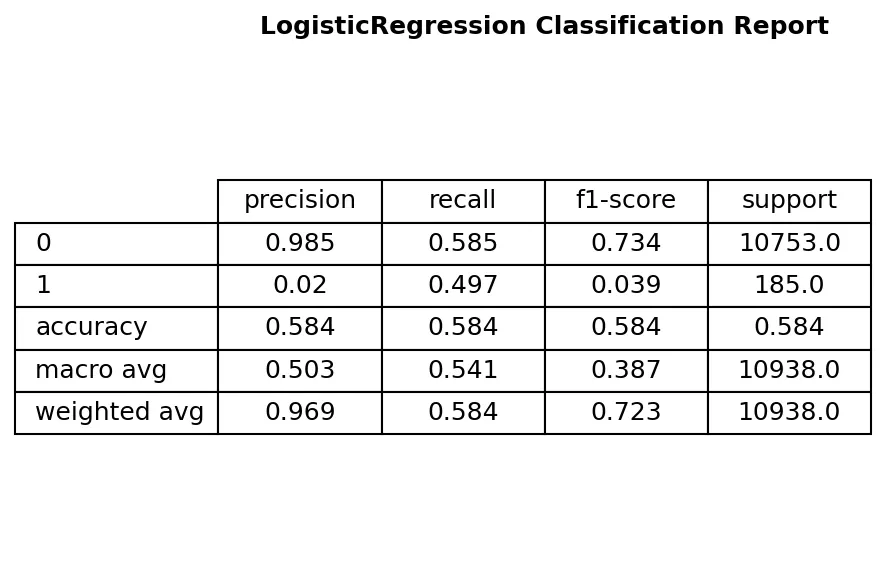

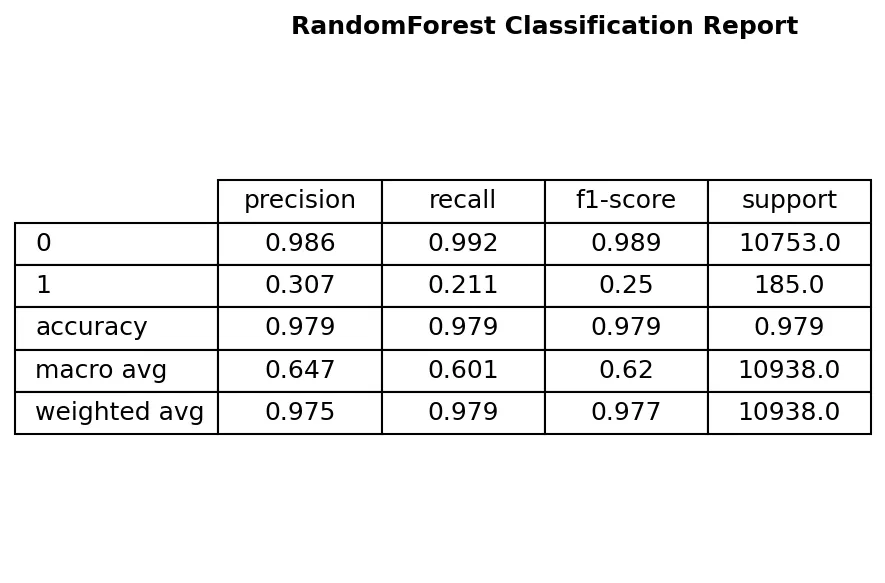

**Prompt: **Please do bivariate and multivariate analysis of the same, i also need classification report, heat map

Terno Response:

Correlation Matrix

Classification Report

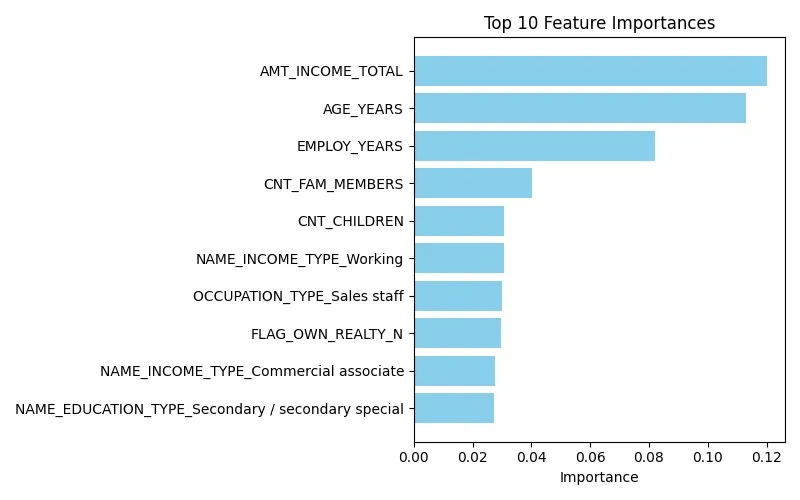

Feature Importance

Insights & Findings by Terno AI

What the Data Says About Credit Defaults

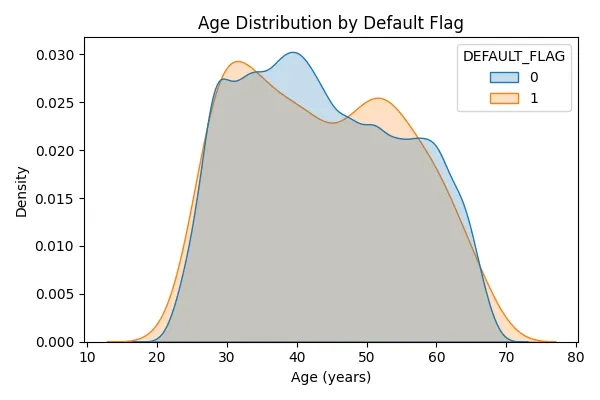

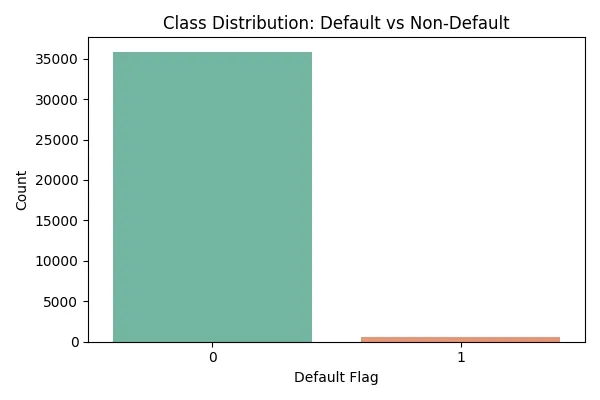

When we set out to explore credit risk, we had two big datasets in hand: one with over 438,000 applicant profiles and another with more than a million monthly balance records. After merging them, we focused on applicants who had ever shown signs of trouble (statuses 2, 3, 4, or 5). That left us with 36,457 people—but only 616 of them were defaulters. Just 1.69%, a tiny fraction, which already hinted at how tough this prediction problem would be.

Cleaning the data brought its own surprises. About a third of applicants hadn’t shared their occupation, so we grouped them under “Unknown.” A few had impossible values in employment days—positive numbers when they should’ve been negative—so we fixed those using the median.

Looking closer, some patterns stood out:

The typical income was around $135,000, and most households had two members.

The median age was 44 years, but those who defaulted tended to be younger—closer to 40 on average.

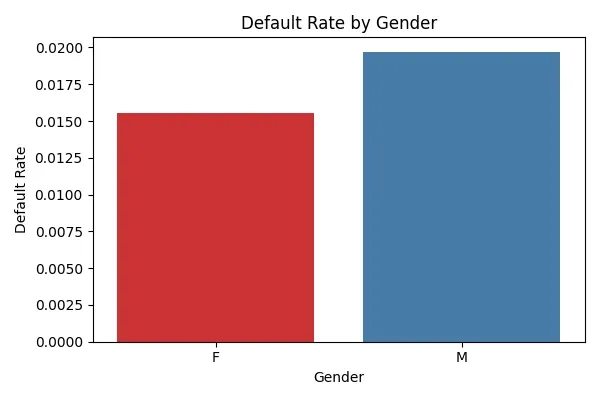

Even gender showed a subtle difference: men defaulted slightly more often (1.8%) than women (1.6%).

Small differences, but together they start painting a picture of who might be at risk.

Key Predictive Factors

When we examined the data, certain patterns became very clear — specific traits consistently indicated whether someone was more likely to default or not.

Higher risk of default

Younger applicants: Individuals at the beginning of their financial journey often exhibit higher risk, likely due to a limited credit history and less financial stability.

Fewer years employed: A short work history can mean income is less predictable, which increases risk.

Lower total income: With less income to rely on, even small financial setbacks can make repayment difficult.

Lower risk of default

Stable, long-term employment: A steady career builds confidence in repayment ability.

Owning real estate: Property ownership often reflects stronger financial stability and responsibility.

Higher income brackets: More income not only eases repayment but also signals stronger financial health overall.

Together, these factors gave us a reliable foundation for predicting who is more likely to default and who is a safer bet for approval.

Recommendations by Terno AI

Based on these insights, Terno AI suggested some simple but powerful rules:

Age and work history matter. Both should be considered in loan approval decisions.

Steady careers pay off. If someone has worked for 10+ years and earns over $200,000, their approval chances are much stronger.

Trust the model. If the predicted risk is under 10%, go ahead and approve — this gives about 95% accurate approvals while keeping risk low.

Conclusion

In this use case, we built a predictive model to assess credit card default risk — all without affecting credit scores.

What made the process smooth was Terno AI. From cleaning the data and exploring it to building the model and evaluating results, the tool handled it all. Its conversational interface made it easy to uncover key factors, while automated insights turned raw numbers into actionable recommendations. You can see the prompts here.

The takeaway? With Terno AI, we could save time, improve accuracy, and make smarter, data-driven decisions.

01 April 2026

Introducing Terno AI Desktop: Your AI Data Scientist, Running Locally

The Enterprise Reality: Why Web-Based AI Falls Short Enterprise environments operate under strict security and infrastructure constraints.

18 March 2026

How terno.ai Transforms Fuel Price Forecasting for Better Decisions

The Mystery of Rising Fuel Prices Every time you pull up to a fuel station in Delhi, Mumbai, Chennai, or Kolkata, you’ve probably noticed something: the numbers on the price board never seem to stop climbing. Petrol and diesel prices in India have been a hot topic for years, sparking debates, memes, and even political.

18 March 2026

Empowering Governments with Rapid Data Insights for Better Decisions

A story of bureaucratic gridlock, data insights, and the moment everything changed Access chat here The Crisis: India's Identity System in Data Purgatory Picture this: It's October 2025. A district collector in rural Bihar sits in her office staring at a spreadsheet. Aadhaar enrollment in her district has been dropping for three months. Is it