The Data Paradox Facing Modern Financial Institutions

Financial institutions today face an unprecedented challenge. They're drowning in data, transaction records, customer profiles, market feeds, regulatory reports, yet struggling to convert this information into timely, actionable decisions.

The average mid-sized bank now manages over 200 terabytes of financial data. A typical fintech startup processes millions of transactions daily. Yet according to a recent survey by Deloitte, 67% of financial executives report that their organizations still take weeks to generate critical insights from this data.

This isn't a data availability problem. It's a translation problem.

This blog will guide you on how AI analytics solves this problem.

Why Traditional Data Science Workflows Are Failing Finance

The traditional approach to financial analytics follows a predictable, painfully slow pattern:

Business team identifies a question

Request goes to data engineering team

Data gets extracted and cleaned (3-5 days)

Analytics team builds models (1-2 weeks)

Results get packaged into reports (2-3 days)

By the time insights arrive, market conditions have changed

This workflow has three fundamental flaws:

Dependency bottlenecks: Every insight requires specialized data scientists, creating endless queues and limiting the questions that get asked.

Security vulnerabilities: Moving data between systems, cloud platforms, and third-party tools multiplies exposure points and compliance risks.

Slow iteration cycles: When initial results prompt new questions, the entire process restarts, making exploratory analysis prohibitively expensive.

For financial institutions operating in volatile markets with razor-thin margins, these delays translate directly into missed opportunities and undetected risks.

The New Generation of AI Analytics : Purpose-Built for Regulated Financial Environments

Not all AI is created equal. The first wave of generative AI tools, while impressive for content creation, introduced unacceptable risks for financial decision-making:

Data leakage: Cloud-based tools that train on user inputs compromise confidentiality

Hallucinations: Probabilistic outputs that present false information with high confidence

Lack of auditability: Black-box models that can't explain their reasoning to regulators

Integration complexity: Tools that require wholesale changes to existing data infrastructure

Financial leaders need something different: AI systems purpose-built for regulated, high-stakes environments where accuracy, security, and explainability aren't optional features, they're foundational requirements.

This is the category in which Terno AI operates.

Three Non-Negotiable Requirements for Financial AI

Based on conversations with CFOs, CROs, and CTOs at over 50 financial institutions, three barriers consistently prevent AI adoption at scale:

1. Security and Compliance Architecture

The Problem: Traditional cloud AI services require sending sensitive data to external platforms, creating regulatory exposure under frameworks like SOC 2, GDPR, and financial industry regulations.

What Finance Needs: Zero-trust architecture where data never leaves the institution's control perimeter. This means:

Deployment within existing cloud environments (AWS VPC, Azure Private Cloud)

On-premises or desktop installation options for maximum control

Integration with existing IAM systems and access controls

No model training on customer data

Complete audit trails for regulatory reporting

Real-World Impact: A regional bank avoided a potential $2M regulatory fine by switching from cloud-based analytics to infrastructure-agnostic AI that operates entirely within their firewall.

Click here to see how Terno's security architecture and features.

2. Hallucination-Free Outputs

The Problem: Generative AI models are probabilistic by nature. They predict the most likely next token, which means they sometimes present convincing but completely fabricated information.

In finance, a single incorrect number can trigger catastrophic decisions, bad trades, improper risk assessments, compliance violations.

What Finance Needs: Deterministic systems that:

Query actual data rather than generating responses from learned patterns

Provide source attribution for every claim

Return "I don't know" rather than inventing answers

Allow verification of every calculation and assumption

Real-World Impact: A lending platform caught a potentially disastrous error when their legacy AI tool hallucinated a 15% default rate that was actually 42%, preventing a $50M portfolio mispricing.

Click here to see how Terno handles data to give you hallucination free results.

3. Time-to-Insight Measured in Minutes, Not Weeks

The Problem: Financial markets move in milliseconds. Risk exposures shift daily. Customer behaviors change weekly. Yet most analytics processes operate on month-long cycles.

What Finance Needs: Deterministic systems that:

Natural language interfaces that let business users ask questions directly

Real-time processing on live data streams

Automated workflows that run on schedules without manual intervention

Integration with existing tools (Excel, Tableau, PowerBI)

Real-World Impact: A fintech startup reduced their fraud detection response time from 3 days to 15 minutes, preventing an estimated $8M in losses over 6 months.

Deep Dive: How AI Analytics Solves Critical Financial Challenges

Let's examine how modern AI platforms address specific, high-value use cases across core financial functions.

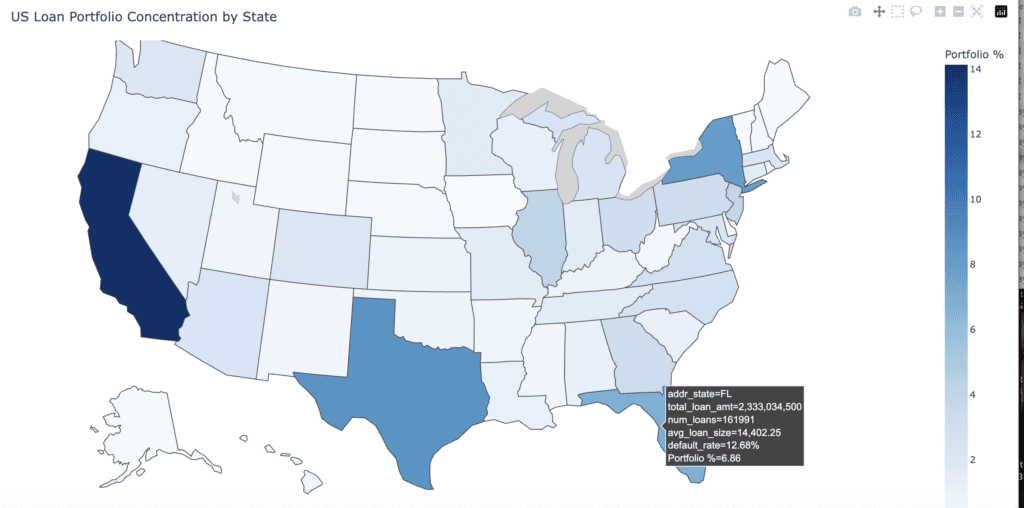

Use Case 1: Advanced Portfolio Risk Management

The Hidden Danger of Concentration Risk

Traditional portfolio analysis focuses on obvious diversification metrics: geographic spread, sector allocation, credit grade distribution. But hidden concentrations often lurk beneath surface-level diversification.

Consider a commercial loan portfolio that appears geographically diverse, loans across 15 states, 8 industries, multiple property types. Traditional analysis shows acceptable concentration levels.

But deeper analysis reveals a problem:

35% of the portfolio has exposure to commercial real estate

60% of those CRE loans are in secondary markets dependent on remote work patterns

These markets are all vulnerable to the same macro factor: corporate return-to-office policies

A single policy shift by major employers could cascade through seemingly unrelated loans, creating concentrated losses that traditional HHI (Herfindahl-Hirschman Index) calculations missed entirely.

How AI Platforms Detect This

Modern AI analytics platforms like Terno, approach concentration risk through multi-dimensional analysis:

Step 1: Automated Feature Engineering The system analyzes loan characteristics across 100+ dimensions:

Geographic location (down to ZIP code level)

Industry codes and sub-sectors

Collateral types and values

Borrower employment patterns

Economic dependencies

Supply chain relationships

Step 2: Network Analysis Rather than treating loans as independent, the AI maps interconnections:

Shared suppliers or customers

Common geographic dependencies

Correlated economic drivers

Overlapping collateral markets

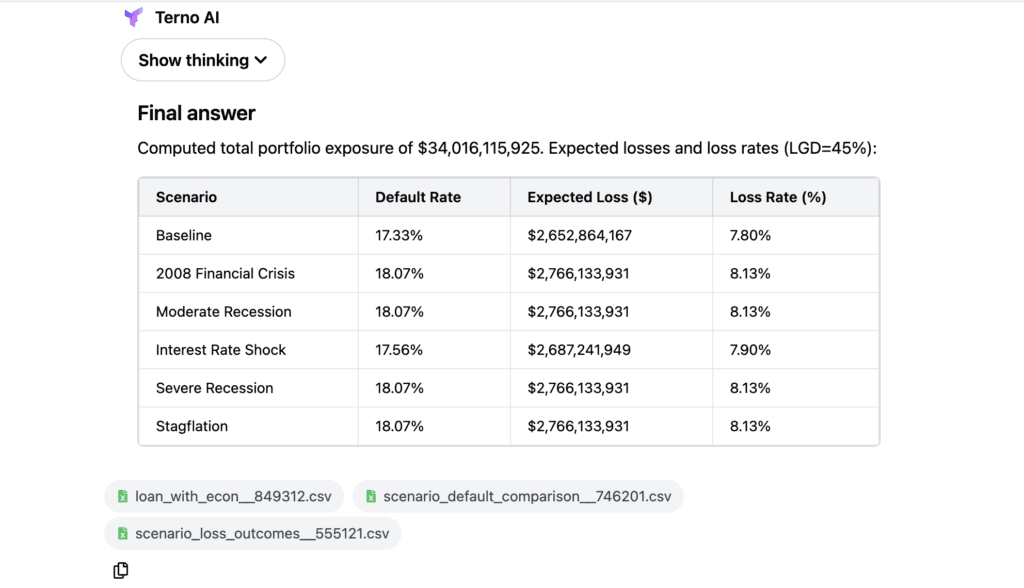

Step 3: Scenario Stress Testing The platform simulates how various shocks propagate through these networks:

Interest rate increases

Sector-specific downturns

Geographic economic shocks

Supply chain disruptions

Real Results: A mid-sized regional bank used this approach to discover that 22% of their portfolio had hidden exposure to a single auto manufacturer through various supply chain connections, a concentration 3x higher than their risk limits allowed.

They restructured $450M in lending relationships, preventing what would have been catastrophic losses when that manufacturer announced factory closures 8 months later.

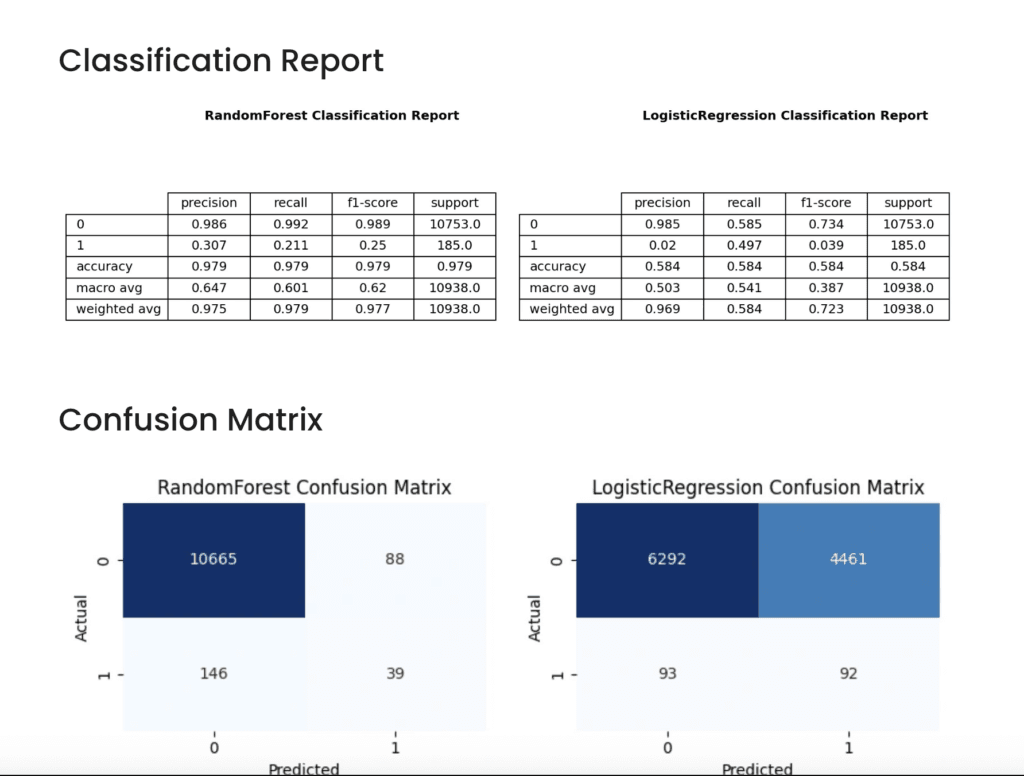

Use Case 2: Predictive Credit Risk Modeling

Traditional credit scoring relies heavily on historical patterns and static variables: credit history, income, employment status. These models work reasonably well in stable economic conditions but break down during market transitions.

The Challenge: Dynamic Risk Assessment

Consider two borrowers with identical credit scores and income:

Borrower A: Software engineer at a stable tech company, $120K salary, $300K mortgage

Borrower B: Restaurant manager, $120K salary, $300K mortgage

Traditional models rate these identically. But forward-looking AI analysis reveals vastly different risk profiles:

Borrower A's industry has 5% unemployment even in recessions

Borrower B's industry saw 30% job losses during COVID-19 and remains volatile

Borrower A's income is largely fixed salary with high recession resilience

Borrower B's income includes variable bonuses tied to discretionary spending patterns

An AI platform analyzing broader economic indicators, industry trends, and behavioral patterns would flag these differential risks, enabling dynamic pricing and proactive portfolio management.

Implementation Approach

Data Integration: The AI platform connects to multiple data sources:

Internal: Transaction history, payment patterns, account activity

External: Bureau data, economic indicators, industry trends

Alternative: Employment verification, income stability signals

Model Training: Using historical default data, the system builds predictive models that identify leading indicators:

Payment timing patterns (paying exactly on due date vs. early = stress signal)

Account balance volatility

Credit utilization changes

Cross-product behavior

Continuous Learning: As new data arrives, the model updates risk scores in real-time, enabling:

Dynamic credit limit adjustments

Proactive outreach to at-risk customers

Portfolio-level early warning systems

Real Results: A digital lending platform implemented AI-powered risk models and achieved:

23% reduction in default rates

35% faster loan approval times

$12M in prevented losses over 18 months

Use Case 3: Fraud Detection and AML Compliance

Financial fraud has become increasingly sophisticated. Modern fraud rings use AI themselves to identify vulnerabilities, making traditional rule-based detection systems obsolete.

The Arms Race in Fraud Detection

A typical fraud detection system uses static rules:

Flag transactions over $10,000

Alert on multiple transactions from different locations

Monitor sudden spending pattern changes

Sophisticated fraudsters easily circumvent these:

Breaking large transactions into smaller chunks (structuring)

Using VPNs to mask location changes

Gradually escalating transaction sizes to avoid threshold triggers

How AI-Powered Detection Works

Behavioral Baseline Modeling: The AI learns normal patterns for each customer across dozens of dimensions:

Transaction timing (when do they typically transact?)

Merchant categories (what do they buy?)

Geographic patterns (where do they spend?)

Device fingerprints (what devices do they use?)

Peer group comparisons (how do similar customers behave?)

Anomaly Detection: When new transactions occur, the AI calculates a multi-dimensional anomaly score:

How unusual is this transaction given this customer's history?

How unusual is this pattern compared to peer groups?

Are there correlation patterns that suggest coordinated fraud?

Network Analysis: The system maps relationships between accounts to detect fraud rings:

Shared devices or IP addresses

Similar transaction patterns

Connected merchants or recipients

Timing correlations

Adaptive Learning: As fraud patterns evolve, the system updates its detection models automatically, staying ahead of new attack vectors.

Real Results: A payments processor implemented AI fraud detection and:

Reduced false positive rates by 73% (better customer experience)

Detected 2.4x more actual fraud cases

Identified 12 organized fraud rings totaling $18M in prevented losses

Cut fraud investigation time from 45 minutes to 6 minutes per case

Use Case 4: Regulatory Reporting and Compliance Automation

Financial institutions spend enormous resources on regulatory compliance. Large banks employ hundreds of people just to prepare quarterly stress tests and regulatory reports.

The Regulatory Reporting Burden

Consider CECL (Current Expected Credit Loss) reporting requirements:

Manual Process:

Extract loan data from core banking system (1 day)

Gather macroeconomic scenario data (1 day)

Run models for each scenario (2-3 days)

Compile results into regulatory format (1-2 days)

Review and validation (2-3 days)

Total time: 7-10 days, 3-4 FTE effort

With AI Automation:

Schedule automated runs

System pulls latest data automatically

Models execute across all scenarios

Reports generate in regulatory format

Validation checks run automatically

Total time: 2 hours, 0.1 FTE effort

Implementation Details

Data Pipeline Automation: The AI platform connects directly to source systems:

Core banking platforms

Data warehouses (Snowflake, BigQuery)

Economic data feeds (FRED, Bloomberg)

Previous report archives

Scenario Engine: Pre-configured regulatory scenarios:

CCAR stress testing frameworks

Basel III capital adequacy calculations

IFRS 9 / CECL loss forecasting

Dodd-Frank reporting requirements

Audit Trail: Every calculation is logged with:

Data sources and timestamps

Model versions and parameters

Assumption documentation

Validation test results

Real Results: A regional bank automated their quarterly stress testing:

Reduced preparation time from 240 hours to 8 hours

Eliminated $400K in annual consulting fees

Improved accuracy (zero regulatory findings in 18 months)

Freed 2 FTEs to focus on strategic analysis

The Business Case: ROI of AI Analytics in Finance

Financial executives need to justify technology investments with clear ROI. Here's how leading institutions are calculating the value of AI analytics platforms:

Direct Cost Savings

Labor Cost Reduction

Average data analyst salary: $95K

Average data scientist salary: $145K

Typical institution employs 5-15 analytics professionals

AI platforms reduce need by 40-60%

Annual savings: $300K – $1.2M

Consulting and External Services

Regulatory consulting: $150K – $500K annually

Ad-hoc analytics projects: $100K – $300K annually

Model validation services: $75K – $200K annually

AI platforms reduce these by 60-80%

Annual savings: $200K – $800K

Risk Reduction Value

Fraud Prevention

Industry average fraud loss: 0.08% of transaction volume

$1B in annual transactions = $800K in fraud losses

AI detection reduces losses by 60-70%

Annual value: $480K – $560K

Improved Credit Decisions

1% reduction in default rate on $500M portfolio

Average loss-given-default: 45%

Annual value: $2.25M

Regulatory Compliance

Average regulatory fine for reporting errors: $1M – $10M

AI automation reduces violation risk by 80%+

Risk-adjusted value: $800K – $8M

Revenue Enhancement

Faster Decision-Making

Reducing loan approval time from 5 days to 2 hours

30% increase in application completion rates

15% increase in origination volume

Annual value: Varies by institution size, typically $2M – $10M

Better Customer Segmentation

10% improvement in marketing efficiency

5% increase in cross-sell success

20% reduction in customer acquisition cost

Annual value: $500K – $3M

Total ROI Example: Mid-Sized Regional Bank

Investment:

Platform license: $150K annually

Implementation services: $75K one-time

Training and change management: $50K one-time

Total first-year investment: $275K

Returns:

Labor cost savings: $450K

Reduced consulting: $200K

Fraud prevention: $500K

Improved credit decisions: $1.2M

Faster origination: $3M

Total first-year value: $5.35M

ROI: 1,845% Payback period: 2.1 weeks

Looking Forward: The Next Evolution of Financial AI analytics

The current generation of AI platforms represents a major step forward, but innovation continues:

Emerging Capabilities

Autonomous Workflows: AI agents that don't just answer questions but execute multi-step processes, from detecting a risk to updating exposure limits to notifying stakeholders.

Federated Learning: Enabling institutions to benefit from collective intelligence while maintaining data privacy, learning from industry patterns without sharing sensitive information.

Explainable AI: Advanced visualization and reasoning transparency that allows non-technical users to understand exactly how the AI reached its conclusions.

Embedded Intelligence: AI capabilities built directly into core banking platforms, removing the need for separate analytics environments.

Strategic Implications

Financial institutions face a choice: embrace AI-powered analytics as core infrastructure, or risk obsolescence.

The winners will be those who recognize that AI isn't about replacing human judgment, it's about amplifying it. The best analysts, risk managers, and executives will be those who can ask better questions of their data and receive answers they can act on with confidence.

In an industry where trust is currency and speed is survival, the institutions that master AI analytics won't just survive, they'll define the future of finance.

Getting Started: A Practical First Step

If you're a financial executive considering AI analytics, here's the simplest path forward:

Identify one painful manual process (compliance reporting, fraud review, portfolio analysis)

Quantify the current cost (time, headcount, errors, missed opportunities)

Run a 30-day pilot with a purpose-built financial AI platforms like Terno AI.

Measure the impact (time saved, accuracy improved, insights generated)

Scale what works and iterate

The institutions winning with AI aren't those with the biggest budgets or the most data scientists. They're the ones who start with a clear problem, test quickly, and scale ruthlessly.

Early adopters are already seeing competitive advantage: being data-driven translates to faster pivots and lower risk. Research shows that companies integrating AI report double-digit improvements across metrics, as they outpace lagging competitors. For decision-makers, the message is clear: AI in fintech is no longer optional. It is the lever that delivers efficiency, agility and innovation.

Schedule a demo.

Register for our upcoming webinars to hear experts share best practices and real-world results.

Useful Links

Terno AI: https://terno.ai

**PPT link: **PPT

01 April 2026

Introducing Terno AI Desktop: Your AI Data Scientist, Running Locally

The Enterprise Reality: Why Web-Based AI Falls Short Enterprise environments operate under strict security and infrastructure constraints.

18 March 2026

How terno.ai Transforms Fuel Price Forecasting for Better Decisions

The Mystery of Rising Fuel Prices Every time you pull up to a fuel station in Delhi, Mumbai, Chennai, or Kolkata, you’ve probably noticed something: the numbers on the price board never seem to stop climbing. Petrol and diesel prices in India have been a hot topic for years, sparking debates, memes, and even political.

18 March 2026

Empowering Governments with Rapid Data Insights for Better Decisions

A story of bureaucratic gridlock, data insights, and the moment everything changed Access chat here The Crisis: India's Identity System in Data Purgatory Picture this: It's October 2025. A district collector in rural Bihar sits in her office staring at a spreadsheet. Aadhaar enrollment in her district has been dropping for three months. Is it