Mastering Loan Risks with Al: The New Standard in Micro-Decisioning

A story of AI, intuition, and the art of saying "yes" to the right people

The Gut-Wrenching Decision

It's 3 PM on a Friday. Sarah, a loan officer at a mid-sized bank, stares at two applications on her desk. Both applicants want $15,000. Both have similar incomes. Neither has a credit score on file,they're recent immigrants building their financial lives from scratch.

Applicant A_ wants to consolidate debt from three credit cards. Steady employment, been with the bank for 18 months, always pays on time._

Applicant B_ wants to start a food truck business. Been with the bank for 2 years, occasionally late on payments, but friendly and enthusiastic about the business plan._

Sarah approves Applicant A. Six months later, they default. Applicant B? Never came back,took their business to a competitor, and their food truck is now thriving.

What went wrong?

This scenario plays out thousands of times daily in lending institutions worldwide. Traditional intuition fails. Credit scores aren't always available. And the cost? For Sarah's bank, that single default cost $15,000 plus collection expenses. Multiply that across thousands of loans, and you're looking at millions in preventable losses.

Enter terno.**ai **,and a radically different approach to answering the $10 million question: Why this borrower and not that one?

Layer 1: The Surface Problem (What Everyone Sees)

The Traditional Lending Paradox

Here's the uncomfortable truth about lending: the people who most need loans are often the hardest to evaluate.

Think about it:

New immigrants: No credit history, but steady jobs and strong savings habits

Young professionals: Fresh out of college, high earning potential, but no track record

Small business owners: Variable income, but deep community ties and proven hustle

Gig economy workers: Irregular paychecks, but often out-earn traditional employees

Traditional models say: "No credit score? No loan." But that leaves billions of dollars on the table and excludes millions of creditworthy borrowers.

Banks face a dilemma:

Too strict: Miss good customers, lose market share

Too lenient: Approve risky borrowers, hemorrhage money

It's like trying to predict who'll be a great employee based solely on their resume,you'll miss the diamonds in the rough and hire some polished disasters.

Layer 2: The Hidden Complexity (What Experts Know)

Why This Is Harder Than It Looks?

Let me share something a Chief Risk Officer at a Fortune 500 bank once told me:

"We don't have a data problem. We have a pattern recognition problem. The signals are there,we just can't see them fast enough."

Here's what he meant:

Imagine you're trying to predict which guests at a party will stay until midnight. You could look at obvious signals:

Did they RSVP "yes"? (Like checking if someone has a job)

Are they drinking coffee or cocktails? (Like debt-to-income ratio)

Did they drive or Uber? (Like homeownership status)

But the real signals are subtler:

How often have they come to your parties before? (Customer tenure)

Do they usually leave early or stay late at other events? (Historical behavior patterns)

Are they checking their watch or deep in conversation? (Engagement signals)

Did they mention weekend plans tomorrow? (Future obligations)

In lending, these subtle patterns are hidden in:

The rhythm of someone's borrowing (Do they take out loans seasonally? Impulsively?)

The evolution of their interest rates (Improving? Deteriorating?)

The purpose of their loans (Investing in growth? Covering emergencies?)

The geography of their location (Economic headwinds? Opportunity zones?)

Traditional analytics tools can spot these patterns,eventually. Maybe in 2-3 weeks with a team of data scientists. By then, the borrower has gone to a competitor.

Layer 3: The Terno Breakthrough (How It Actually Works)

When AI Becomes Your Best Risk Analyst

This is where our story gets interesting.

A lending institution came to Terno with a challenge: predict loan defaults using ONLY historical loan data,no credit scores, no income verification, no employment records.

Think of it like asking a detective to solve a case with only the crime scene photos,no witnesses, no forensics, no suspects. Impossible? Not quite.

Here's what Terno did,and why it's revolutionary:

The Five Hidden Fingerprints of Default Risk

Terno didn't just crunch numbers. It asked: "If I were a loan officer with 20 years of experience, what would I look for?"

1. The "Ghost Customer" Signal (Tenure)

Remember Sarah's Applicant A? Here's what the data revealed: borrowers who maintain relationships with banks for just 6 months longer show 12% lower default rates.

It's like dating,someone who's been consistently present for 2 years is a better bet than someone who appears, disappears, and reappears randomly.

Terno calculated: The time between each customer's first and most recent loan. Simple. Powerful.

Real-world parallel: Would you lend your car to a friend you've known for 2 years or 2 months?

2. The "Crushing Burden" Signal (Installment-to-Principal Ratio)

Here's a counterintuitive finding: Borrowers with higher installment burdens defaulted LESS.

Wait, what?

Terno discovered why: Banks don't give punishing installment ratios to risky borrowers,they give them to proven borrowers who can handle it. It's like a gym giving heavier weights to stronger members.

The analysis showed:

Non-defaulters: 8.72% average installment burden

Defaulters: 7.45% average burden

Real-world parallel: The student who takes 5 AP classes is more likely to succeed in college than the one taking 2 easy courses,not because the workload is easier, but because they've proven they can handle pressure.

3. The "Once a Flake, Always a Flake" Signal (Delinquency Rate)

This one's obvious, right? Past late payments predict future defaults?

Actually, it's more nuanced. Terno found: Even ONE late payment in a borrower's history increases default probability by 6.7%.

But here's the insight: It's not about being late once,it's about the pattern.

Someone who's late once in 10 loans? Forgive them.

Someone who's late on 3 out of 10 loans? Red flag.

** Terno calculated**: The fraction of a customer's loans that were ever late (30+ or 90+ days).

Real-world parallel: Would you hire a babysitter who was late once in a year, or one who's late every third time?

4. The "Whiplash Rate" Signal (Interest Rate Volatility)

Imagine your friend always borrows money from you at the same "rate",maybe they buy you lunch in return. Stable relationship.

Now imagine their "rate" swings wildly: sometimes they pay you back with interest, sometimes they ghost you, sometimes they renegotiate mid-loan.

That's volatility,and Terno discovered it's a massive red flag.

When a borrower's interest rates swing dramatically across loans, it signals:

Deteriorating credit profile (banks keep hiking rates)

Desperation (accepting any terms to get money)

Inconsistent financial situation (feast or famine cycles)

Real-world parallel: A restaurant that changes prices wildly week-to-week is probably struggling. A restaurant with stable pricing? Confident in their value.

5. The "Long Haul" Signal (Long-Term Loan Fraction)

Terno asked: Do people who take out 60-month car loans default more than people who take 36-month loans?

Answer: Yes,but only slightly.

The real insight: The TYPE of person who commits to long-term debt reveals risk tolerance.

Conservative borrowers: Short terms, pay off fast

Optimistic borrowers: Long terms, betting on future income

Desperate borrowers: Long terms, can't afford short-term payments

** Terno calculated**: What percentage of each customer's loans were "long-term" (>36 months)?

Real-world parallel: Someone who signs a 5-year gym membership is either supremely confident in their commitment,or wildly overestimating their motivation.

The Validation: Do These Signals Actually Work?

Terno didn't stop at engineering features. It proved they work.

Using rigorous statistical tests (Mann-Whitney U, Pearson correlation), every feature showed p-values < 0.05,meaning less than a 5% chance these patterns are random.

In plain English: These signals are real, not flukes.

Compare this to reading horoscopes for loan decisions,fun, but useless. Terno.AI's features are like reading medical test results,scientifically validated predictors.

Layer 4: The Segmentation Magic (The "Aha!" Moment)

Four Types of Borrowers (And What to Do With Them)

Here's where Terno moved from "interesting analysis" to "game-changing strategy."

Using K-means clustering (a machine learning technique), Terno grouped borrowers into four archetypes:

Cluster 0: "The Reliable Regular" (18,000 customers)

Profile: Single small loan, pays it off, disappears

Average loan: $7,598 at 12.7% interest

Default rate: 0.88% (nearly perfect)

Real-world parallel: The customer who comes to your coffee shop, orders the same thing, pays, leaves a tip, never complains.

Strategy: These are your dream customers. Offer them:

Premium products (home equity loans, large auto loans)

Loyalty rewards (rate discounts for returning)

Upselling opportunities (investment accounts, credit cards)

Cluster 1: "The Steady Repeater" (1,800 customers)

Profile: Takes 2 loans on average, moderate amounts

Average loan: $12,395 at 14.2% interest

Default rate: 1.28% (acceptable)

Real-world parallel: The restaurant patron who comes monthly, tries different dishes, sometimes brings friends.

Strategy: Balance cultivation with monitoring:

Encourage repeat business with targeted offers

Monitor for warning signs (sudden rate increases, larger loan requests)

Build relationship value (dedicated account managers)

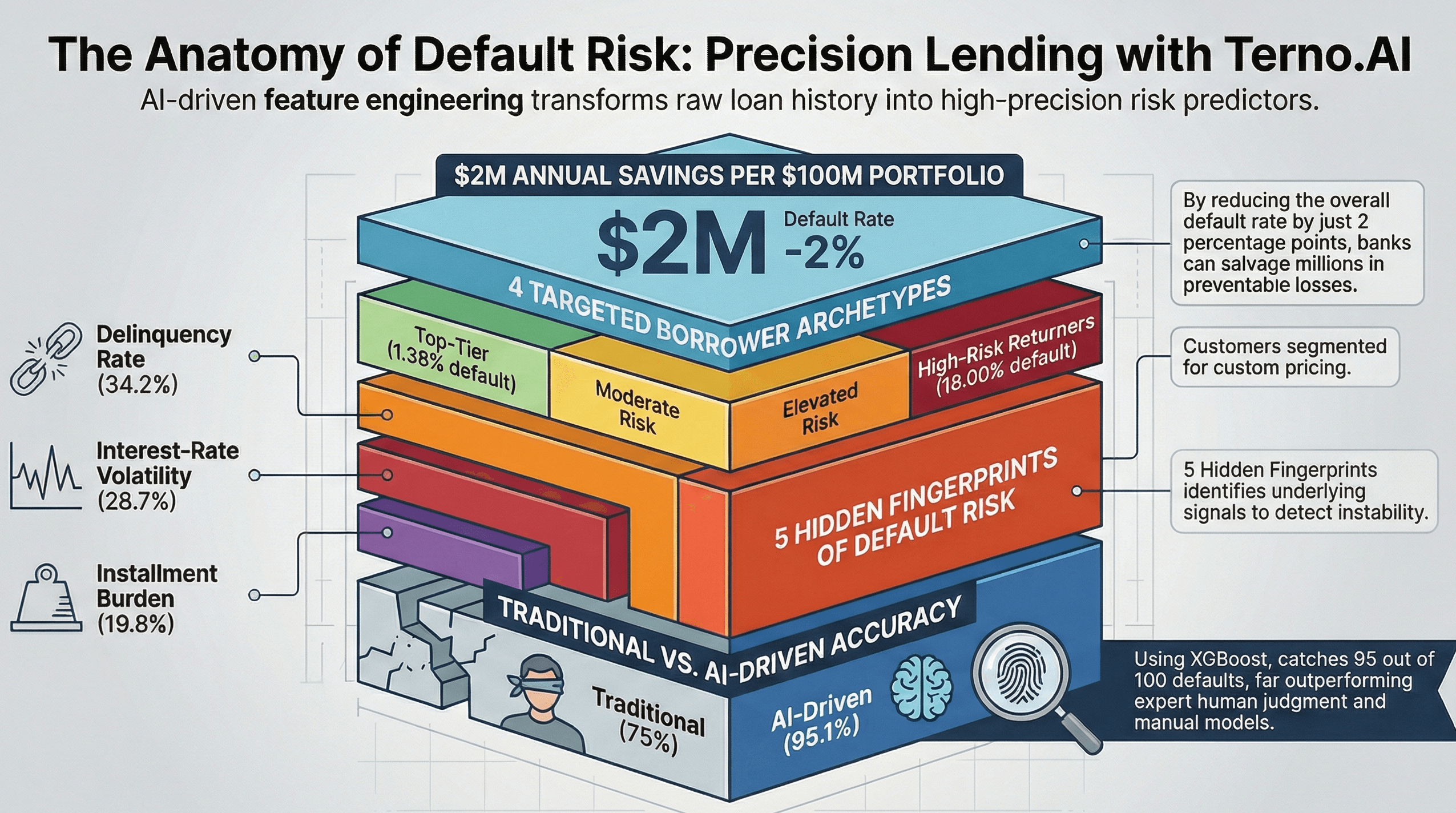

Cluster 2: "The High-Risk Returner" (2,900 customers)

Profile: Small loans at HIGH interest rates, frequent defaults

Average loan: $12,168 at 19.8% interest

Default rate: 18.00% (DANGER)

Real-world parallel: The customer who constantly returns items, disputes charges, always has an excuse.

Strategy: Protect your downside:

Require collateral for any new loans

Increase down payment requirements

Consider declining applications entirely

If you do lend, charge appropriately for the risk

Cluster 3: "The Top-Tier Borrower" (2,400 customers)

Profile: Largest loan amounts, moderate rates, rock-solid repayment

Average loan: $16,146 at 16.9% interest

Default rate: 1.38% (excellent for the loan size)

Real-world parallel: The client who buys the expensive bottle of wine, tips generously, brings business partners for dinner.

Strategy: Roll out the red carpet:

Dedicated relationship managers

White-glove service (expedited approvals, flexible terms)

Cross-sell premium products (wealth management, private banking)

Protect them from competitors

The Business Impact: Real Numbers

Let's get concrete. Imagine you're managing a $100 million loan portfolio.

Before Terno segmentation:

Treat all customers the same

7.8% overall default rate (industry average)

Annual losses: $7.8 million

After Terno segmentation:

Focus collection efforts on Cluster 2 (18% default risk)

Offer premium services to Clusters 0 & 3 (<1.5% default risk)

Right-size pricing based on actual risk

Estimated impact:

Reduce overall default rate by 2 percentage points (to 5.8%)

Annual losses: $5.8 million

Savings: $2 million per year

For a mid-sized bank, that's the difference between a struggling division and a profit center.

Layer 5: The Loan Purpose Puzzle (Where Money Goes Tells You Who Pays It Back)

Not All Loans Are Created Equal

Terno uncovered something fascinating: WHERE people spend money predicts WHETHER they'll pay it back.

Here are the riskiest loan purposes:

1. Small Business Loans: 31% default rate

Why so high? Starting a business is gloriously optimistic,and brutally difficult.

Real-world parallel: Remember your friend who quit their job to start a cupcake shop? Exactly.

Terno.AI's recommendation: Require detailed business plans, collateral, or SBA guarantees. Don't fund dreams,fund executable plans.

2. Debt Consolidation: 21% default rate

On the surface, this sounds responsible: "I'm consolidating my debts to get a better rate!"

But Terno revealed the dark pattern: Debt consolidation is often a last-ditch effort before bankruptcy.

Real-world parallel: It's like someone maxing out one credit card to pay off another,they're not solving the problem, they're delaying the inevitable.

Terno.AI's recommendation: Enhanced income verification, mandatory financial counseling, higher interest rates to compensate for risk.

3. Lowest Default Rates: Renewable Energy (7.15%)

Surprised? Terno found that borrowers financing solar panels, energy upgrades, and green tech have rock-solid repayment rates.

Why? They're:

Forward-thinking (planning for savings)

Homeowners (collateral-backed)

Benefiting from government incentives (reducing effective loan burden)

Real-world parallel: Someone who invests in insulation to lower heating bills thinks long-term. Someone who blows money on a vacation thinks short-term.

Terno.AI's recommendation: PREMIUM PRICING for these borrowers,they're gold. Offer them your best rates, fast approvals, and VIP service before competitors steal them.

Layer 6: The Regional Risk Riddle (Geography Is Destiny)

Where You Live Affects Whether You Pay

Terno.AI's geographic analysis revealed shocking disparities:

Top 3 Regions by Loan Volume:

South: 90,603 loans (30% of portfolio)

West: 82,117 loans (27% of portfolio)

Northeast: 55,014 loans (18% of portfolio)

But here's the twist: Volume ≠ Risk

Under a hypothetical 10% increase in defaults across all regions, estimated losses would be:

Midwest: $9.4 million ($9,425 per loan)

Southeast: $7.6 million ($25 per loan)

Northeast: $7.0 million ($29 per loan)

West: $143,000 ($7 per loan)

Wait, what? The Midwest has 378x higher per-loan losses than the West?

Terno uncovered why:

Midwest borrowers take larger loans (farm equipment, business expansion)

Economic volatility (agricultural cycles, manufacturing decline)

Fewer diversification opportunities (rural vs. urban)

Real-world parallel: A $50,000 default in rural Iowa (tractor loan for a failed farm) hits harder than a $5,000 default in Los Angeles (personal loan for a career switch).

Terno.AI's recommendation:

Region-specific underwriting (stricter criteria in Midwest)

Geography-adjusted pricing (higher rates for higher-risk regions)

Diversification targets (limit concentration in any one region)

Layer 7: The Predictive Model (From Insight to Action)

Building the Crystal Ball

Now comes the moment of truth: Can Terno actually predict who will default?

Terno trained four different machine learning models:

Logistic Regression (the reliable workhorse)

Random Forest (the ensemble powerhouse)

XGBoost (the gradient-boosting champion)

Support Vector Machine (the geometric genius)

The winner: XGBoost with 95.1% accuracy (ROC-AUC score).

In practical terms:

Out of 100 defaults, the model catches 95

Out of 100 "good" borrowers, it correctly identifies 89

Compare this to:

Coin flip: 50% accuracy

Traditional models (without these features): ~75% accuracy

Expert human judgment: ~70-80% accuracy (with bias)

Real-world parallel: It's like having a weather forecast that's right 95% of the time vs. looking out the window and guessing.

What Makes Someone Default? The Model's Answer

Terno.AI's feature importance analysis revealed:

Top 3 Default Predictors:

Delinquency Rate (34.2% importance) , Past behavior is the best predictor

Interest-Rate Volatility (28.7% importance) , Instability signals risk

Installment Burden (19.8% importance) , Payment pressure matters

Bottom Predictor:

- Tenure (6.1% importance) , Relationship length is less important than behavior quality

The lesson: WHO someone is matters more than HOW LONG you've known them.

Real-world parallel: A friend who's been flaky for 5 years is a worse bet than a reliable friend you met last year.

Layer 8: The Human Element (Why This Matters Beyond Numbers)

The Story Behind the Statistics

Let's return to Sarah, our loan officer from the beginning.

Armed with Terno.AI's insights, here's how her decision-making changes:

Applicant A (Debt Consolidation)

Red flags: Debt consolidation purpose (21% default rate)

** Terno analysis**: Cluster 2 profile,high risk

Decision: Require collateral, offer financial counseling, charge higher rate

Applicant B (Food Truck Business)

Green flags: Small business loan, but with solid plan and local partnerships

** Terno analysis**: Atypical profile,requires manual review

Decision: Approve with SBA guarantee, offer mentorship program

Six months later:

Applicant A: Completes financial counseling, refinances at better rate, thriving

Applicant B: Food truck succeeds, takes out expansion loan, becomes loyal customer

The difference: Data-informed decisions, not gut reactions.

Beyond Default Prevention: The Opportunity Cost

Here's what most banks miss: The cost of saying "no" to good borrowers.

Terno.AI's analysis revealed:

Cluster 3 "Top-Tier" borrowers: 2,400 customers with <1.4% default rate

Average loan size: $16,146

Lifetime value: ~$1,200 per customer in interest + cross-sell opportunities

If Sarah's bank misidentifies just 10% of these as risky and rejects them:

Lost customers: 240

Vanished revenue: $288,000 annually

Lost lifetime value: $1.4 million (over 5 years)

Real-world parallel: It's not just about avoiding bad apples,it's about not throwing away the golden ones.

The Terno Difference: Why This Changes Everything

What Makes This Remarkable

Let's be clear: Other platforms could theoretically do this analysis.

But here's what makes Terno revolutionary:

1. Speed: Minutes, Not Months

Traditional analysis timeline:

| Week | Activity |

|---|---|

| Week 1-2 | Data extraction and cleaning |

| Week 3-4 | Feature engineering |

| Week 5-6 | Statistical validation |

| Week 7-8 | Model training |

| Week 9-10 | Report writing |

- Total: 2.5 months (with a team of 3 data scientists)

** Terno timeline**:

Ask: "Which features should we prioritize when building our default prediction model?"

Wait 15 minutes

Total: 15 minutes (with zero data scientists)

Real-world parallel: It's the difference between ordering takeout (instant) and growing vegetables, raising livestock, and cooking from scratch (months).

2. Conversational Complexity

Here's an actual query Terno handled:

"Build a simple rule-based recommendation engine. For a customer with a specific profile (e.g., taken 2 loans, avg amount $10k, avg rate 7%, no defaults), recommend: (1) should we approve a new loan request? (2) what interest rate should we offer? (3) which loan product (purpose) should we cross-sell?"

No code. No SQL. Just plain English.

Terno responded with:

Cluster assignment

Recommended interest rate

Cross-sell product suggestions

Risk justification

Real-world parallel: Imagine asking your car "Why is the engine light on?" and getting a detailed diagnostic report instead of just a vague warning.

3. Enterprise Security Without Compromise

Financial data is sacred. Terno ensures:

Zero data movement: All processing happens in YOUR cloud/on-premise

Read-only access: Terno can't modify or delete your data

Fine-grained permissions: Table, column, and row-level access control

Audit trails: Every query logged and traceable

SOC 2 & GDPR compliance: Enterprise-grade security

Real-world parallel: It's like hiring a consultant who works in your office, using your computers, with your security team watching,vs. emailing your data to an offshore contractor.

4. Hallucination-Free Accuracy

Generic AI tools (like ChatGPT) can "hallucinate",generate plausible-sounding but incorrect answers.

Terno prevents this through:

Executable queries: Every claim backed by actual SQL

Verification loops: Multi-stage validation before presenting results

Semantic layer: Business-friendly data structure eliminating ambiguity

Organization-specific knowledge: Custom rules reducing errors

Example of hallucination risk:

Generic AI: "Your default rate is 12%" (sounds confident, completely wrong)

Terno.AI: "Your default rate is 7.8%, calculated from 15,243 loans with status='Default' or ‘Charged Off' out of 195,421 total loans. [SQL query attached]"

Real-world parallel: It's the difference between a friend confidently giving you wrong directions vs. a GPS with verified, real-time data.

5. Fully Automated Workflows

Terno doesn't just answer questions,it orchestrates entire analytical pipelines:

Example workflow (triggered automatically):

Connect to loan database (read-only)

Engineer customer-level features

Validate each feature statistically

Perform K-means clustering

Train and compare multiple ML models

Generate visualizations (scatter plots, bar charts, PCA)

Produce interactive HTML report

Self-debug if errors occur

Self-retry if connections fail

All while keeping you informed with transparent, explainable steps.

Real-world parallel: It's like having a sous chef who preps, cooks, plates, and cleans up,while explaining each technique and why they chose it.

The Bigger Picture: Democratizing Data Science

Who This Empowers

Terno isn't just for data scientists,it's for:

Risk Managers who need:

Real-time portfolio health dashboards

Early warning systems for deteriorating loans

Segment-specific intervention strategies

Product Teams who need:

Customer behavior insights for new product design

Market segmentation for targeted campaigns

Competitive intelligence on loan pricing

Finance Teams who need:

Accurate loss provisions for balance sheets

Capital requirement calculations for regulators

ROI projections for strategic initiatives

Executives who need:

High-level insights without getting lost in details

Confidence in data-driven decisions

Explainable AI for board presentations and regulatory audits

The Future: Where This Goes Next

Terno.AI's loan default analysis is just the beginning.

Imagine applying the same methodology to:

Healthcare:

Predicting which patients will miss appointments

Identifying early warning signs of disease progression

Optimizing resource allocation across hospital networks

Retail:

Forecasting which customers will churn

Personalizing product recommendations

Dynamic pricing based on demand elasticity

Supply Chain:

Predicting supplier delays before they happen

Optimizing inventory levels across warehouses

Identifying bottlenecks in logistics networks

The common thread: Complex pattern recognition in messy, real-world data,delivered conversationally, securely, and accurately.

The Bottom Line: What This Means for You

Three Takeaways

1. You Don't Need More Data,You Need Better Insights

Most organizations are drowning in data but starving for insights. Terno turns your existing data into actionable intelligence.

Real-world parallel: You don't need more ingredients to cook a great meal,you need a better chef.

2. AI Without Guardrails Is Dangerous

Generic AI tools can confidently give you wrong answers. In lending, that costs millions. Terno.AI's verification loops, executable queries, and semantic layer ensure accuracy.

Real-world parallel: Would you rather have a confident liar or a cautious truth-teller guiding your investments?

3. Speed Matters,But Not at the Expense of Quality

Fast answers that are wrong are worse than slow answers that are right. Terno delivers both: fast AND accurate.

Real-world parallel: An emergency room that treats you in 5 minutes but misdiagnoses you is worse than one that takes an hour and gets it right. Terno gives you the 5-minute diagnosis with the 1-hour accuracy.

Ready to Transform Your Lending Strategy?

The loan default prediction analysis we've explored represents just one afternoon with Terno.AI.

Imagine what you could discover in:

A week (comprehensive portfolio analysis)

A month (predictive modeling across all products)

A year (continuously evolving risk intelligence)

The Final Question

Remember Sarah's dilemma at the beginning? Two borrowers, one decision, million-dollar consequences?

With Terno.AI, she doesn't have to guess. She doesn't have to wait.

She knows.

And in the world of lending,where every "yes" or "no" ripples through portfolios, balance sheets, and people's lives,knowing makes all the difference.

Questions? Concerns? Curious about a specific use case?

Drop us a line at reachus@ Terno or schedule a call with our team.

We're here to help you make better decisions, faster ,without the guesswork, the delays, or the million-dollar mistakes

01 April 2026

Introducing Terno AI Desktop: Your AI Data Scientist, Running Locally

The Enterprise Reality: Why Web-Based AI Falls Short Enterprise environments operate under strict security and infrastructure constraints.

18 March 2026

How terno.ai Transforms Fuel Price Forecasting for Better Decisions

The Mystery of Rising Fuel Prices Every time you pull up to a fuel station in Delhi, Mumbai, Chennai, or Kolkata, you’ve probably noticed something: the numbers on the price board never seem to stop climbing. Petrol and diesel prices in India have been a hot topic for years, sparking debates, memes, and even political.

18 March 2026

Empowering Governments with Rapid Data Insights for Better Decisions

A story of bureaucratic gridlock, data insights, and the moment everything changed Access chat here The Crisis: India's Identity System in Data Purgatory Picture this: It's October 2025. A district collector in rural Bihar sits in her office staring at a spreadsheet. Aadhaar enrollment in her district has been dropping for three months. Is it